The Heavy Weather Report - 2006

![]()

In January of 2006 I wrote an essay on the coming economic crisis, adding myself to a growing list of doom-sayers that have accumulated over the past 30 years and have become especially strident of late. I distributed it to family and friends, urging them to:

Exit currencies, real estate, equities and bonds.

Invest in precious metals, commodities and energy, and

Move their assets offshore.

Here is the text of that essay, essentially unchanged. I will present the results of my own research, the alternatives I considered, and the actions I have taken. Your mileage may vary. I urge you to do your own research and make your own decisions as I have.

In January of 2007 I reviewed the previous year relative to this essay and extended projections to the next, with extensive notes on the underlying economics. The 2007 Heavy Weather Report is here.

Some of you have already guessed that my subject is an impending economic crisis. I'll give you the opportunity to hit the delete button if this is too much for you by summarizing the points I intend to make:

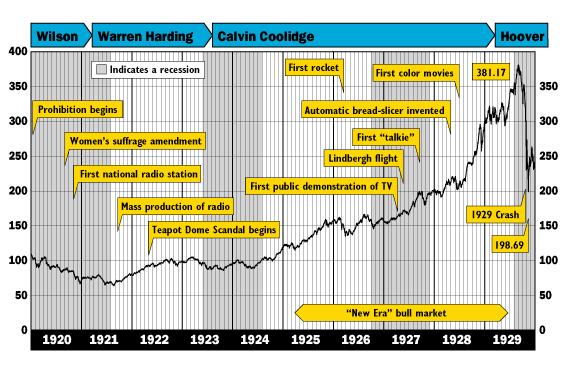

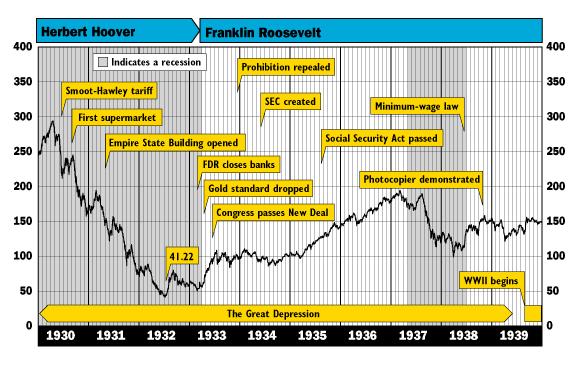

The 2000 stock market crash is not over, the apparent partial recovery is illusory, temporary, and has just about run its course.

Your government has not been completely honest with you about economic indicators like unemployment, inflation, and GDP. Things are worse than they appear.

In the next 1-2 years we will experience the beginning of an economic downturn similar to the 1970's, and possibly as severe as the 1930's. Recovery will be painful and require on the order of 10 more years.

The economic landscape today is very different from those earlier crises. The next one will have some similarities, but will run a significantly different course.

The consequences will likely include high interest rates, serious unemployment, recession, stagnant wages, and double-digit inflation (so-called 'stagflation').

Those whose wealth is in the form of dollar-denominated assets may be impoverished. This includes specifically stocks, bonds, and real estate. The Dow will bottom out at something like 1/3 of it's current value in inflation adjusted terms.

We are now several years into a commodities boom. You ain't seen nuthin' yet. For the next 6-10 years commodities will be the big winners. This includes specifically energy, metals in general, and precious metals in particular. Gold will peak to at least $3,000/oz. It may or may not fall back to the 1500-2000 range.

(Put on your tinfoil hat now.) A 1930's-style depression is more than possible but less than likely. When things get that bad, governments (including ours) have historically taken draconian measures: currency exchange controls, wage and price regulation, restricted access to bank accounts, forced conversion of assets, confiscation of private gold and silver, even travel restrictions. You shouldn't base your plans on any of this happening, but you should have a 'Plan B' in place to deal with them if you see them coming. (You can take that tinfoil hat off now.)

Wolf! Wolf!

Please understand, I'm not running around in circles screaming “We're All Freakin Doomed!” like many of the gold enthusiasts I know. Frankly I got hoarse doing that for the last 40 years. The sky has displayed an annoying tendency not to fall. Civilization will not break down into savage anarchy. Your electricity will still work, though it may be several times more expensive. The US will still exist, though perhaps not as a superpower. My message is that we probably have some rather heavy weather ahead, but there are ways to profit rather than suffer from it should it occur, ways that will leave us no worse off (even a little better off) even if it doesn't.

Are you still with me? I didn't scare you off with that tinfoil hat stuff? Good. I had second and third thoughts about including that last item. OK, let's take on these things in a little more detail.

The 2000 stock market crash is not over, the apparent partial recovery is illusory, temporary, and has just about run its course.

This partial recovery followed by a further fall is a very common market phenomenon. We see it in other economic downturns, especially in 1930.

It's called the 'Dead Cat Bounce', or the 'Double Top' or the 'Bear Market Rally'. What's been fueling this recent bounce has been consumer spending, spending money they don't really have, money from credit cards and home equity/refinance loans, loans from easy credit and a false real estate boom, both driven by low interest rates, money ultimately created out of thin air by the fed.

The economic fundamentals are so bad, the question is not "will there be a downturn?", but "why hasn't it happened sooner?". (The short answer to that is "the USD has been the world's reserve currency", but more on that later.) So, the 2000 dotcom crash is still going on, masked by low interest rates, 2 trillion dollars of newly created government debt since 2001,

and changes in the way major economic indicators, like unemployment and inflation, are calculated (more on that later). Then there's the trade deficit.

That's foreigners accepting our IOUs for goods made cheap after we exported our jobs and manufacturing ability to them. This makes us feel rich while we're just running up a tab.

Your government has not been completely honest with you about economic indicators like unemployment, inflation, and GNP. Things are worse than they appear.

This should come as no surprise. I hate to come off like a conspiracy theorist, but the facts are that there has been a series of changes in the way what they call 'leading economic indicators' are calculated. The effect of these changes has been to make economic conditions appear better than they are. This has affected the published figures on unemployment, inflation, and GNP. For example: unemployment used to mean how many people wanted a job but couldn't find one. Now it means how many people are drawing unemployment compensation. Those who gave up looking, and those whose unemployment has run out are not counted. the currently published figure is about 4%. Calculated the way it was in 1929, that would be 12%.

Another example: CPI, the Consumer Price Index, is the primary measure of inflation. But it does not count the cost of the things we spend most of our income on, housing, energy, medical care. Curiously these are also the things that have increased the most. Then there is a pathetic little gimmick called the 'hedonic adjustment'. This is the theory that it doesn't matter if steak gets more expensive because you'll just shift to hamburger, and that's cheap. So your cost of living didn't really go up, see? You could carry this out to some sort of Orwellian endgame where we're all living in tents , wearing gunny sacks, and eating dog-food. but it's alright cuz the CPI is flat. The current inflation figure given out is 3.6%, figured the old way: 6.1%. Without this chicanery, social security payments (which are indexed to the CPI) would have to be almost twice as high.

Similar games are played with the GNP. Did you know that if you own the house you live in, you are your own landlord? And part of your income is from renting your home to yourself? That pseudo-income is counted as part of the GNP. Gee. Want more details? Check this out: https://secure.goldmoney.com/en/commentary/2006-03-07.html

One final note on this subject: Last month (March 2006) The Fed stopped publishing M3, the measure of how much US money is in circulation. From the M3, we know that son-of-Bush has tripled the money supply. Amazing. Printing money faster than the country creates real wealth is where inflation comes from. But now that the printing rate will be unknown, the questionable inflation and wealth figures will be harder to check. Is there a conspiracy to sugar-coat unpleasant economic realities? It hardly matters, they are sugar-coated.

In the next 1-2 years we will experience the beginning of an economic downturn similar to the 1970's, and possibly as severe as the 1930's. Recovery will be painful and require on the order of 10 more years.

How do we know a major downturn is immanent? There are lots of signals. Exponentially increasing government debt at 3 X GDP usually precedes a currency collapse. An inverted government bond yield (short-term bonds earn higher than long term bonds) usually precedes a recession.

The countries that have been financing our twin deficits (China, Japan, OPEC members) are cutting back and moving from dollars to Euros and gold as currency reserves (This is a very, very bad thing). Others, like Russia, are doing the same. There is a movement among Asian countries to create a trading currency alternative to the dollar, and another in the middle east to revive gold and silver-based traditional Islamic currencies, the Dirham and Dinar. There is much talk, and some action towards making a market for oil in Euros instead of dollars in Russia, Syria, Iran, Venezuela, Iceland, and others. This is another very bad thing ... for us.

The real estate boom that replaced the dotcom boom has clearly topped out and is starting to fall back with nothing obvious to replace it. Major industries like airlines and auto-makers are going bankrupt or just laying off workers 30,000 at a whack.

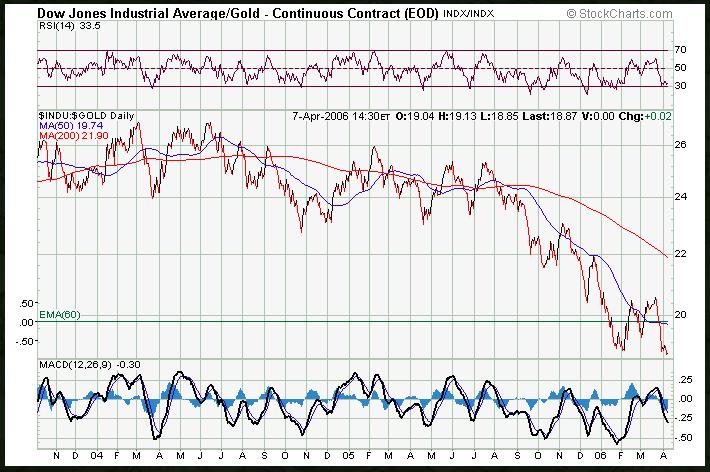

You might look at the Dow, the S&P500, the NASDAQ, and think all is roses on Wall Street, they are all going up, not great, but up. Wrong. In inflation-adjusted terms, the Dow has shown an average annual 3% loss over the last 4 years. Want to know a better measure of stock market health? Let me introduce you to the Dow/gold ratio. The Dow is the total price in dollars of a selected basket of NYSE stocks. The Dow/gold ratio is that price in gold ounces, said another way: how much gold it takes to buy the Dow. The free market purchasing power of gold changes very little over time. It's dollar price varies a great deal, but this is mostly change in the purchasing power of dollars, not a change in the purchasing power of gold. Gold is the best objective measure of value around the world and over time. So the Dow/gold ratio is a currency-independent measure of the stock market. At the height of the dotcom boom it was at 40. 7 months ago, the Dow/gold ratio began dropping like a rock. Now it's below 20 and falling. This tells you it's a bad time to own stocks, to say the least. It also tells you the market is in freefall, regardless of what the Dow seems to say. 15 will be a watershed threshold. At the bottom of a major crash, this ratio may approach 1 or 2.

We have a ways to go but we're getting there fast. About 4 years at the current rate, but these things tend to fall off a cliff suddenly at some point so it's impossible to say exactly when. But we can say with some confidence that we will reach the edge of that cliff in somewhere between 6 months and 2 years. Then it's a swift, 3-6 month trip to the bottom.

Why should we expect it to be any worse than recent recessions? Many of the reasons I cited above for immanence are unique in US history, and not in a good way. Especially the hard-to-even-visualize dual deficits and the falling international confidence in the dollar as a reserve and trading currency. Never before have we been in a war and decreased taxes, rather than increasing them to pay for it. We have created more government debt over the last 10 years than in the previous 200. We used to be the world's biggest lender. Now we are the world's biggest borrower. The only thing between us and national bankruptcy is our privileged position as issuer of the world's reserve currency. If that should change, we are toast. And there are now signs of such a change. It may happen slowly. or it may be a sudden landslide as social/economic events often are. My vote is for a gradual change over months or years, then a sudden rush-for-the-exits over weeks or months. Nobody wants a disorderly flight from the dollar, they hold to many of them. But like any lender, at a certain point you have to just write off a bad debt and stop throwing good money after bad. I suspect there won't be much warning about this, if it happens.

The economic landscape today is very different from those earlier events. The next one will have some similarities, but will run a significantly different course.

In the previous section I mentioned some ways in which our current situation is unique. Here are some other ways the economy functions differently that it did in the 70's. Today, we have the Internet. When some Ayatollah issues a fatwa in Tehran, oil prices shift all over the planet literally in minutes. Markets are instantly affected by events all over an increasingly unpredictable planet. Today, we have globalization. Economies are interconnected and interdependent, blurring their boundaries, making them more complex and unpredictable. Today we have the small private investor. The stock market used to be the domain of investment bankers with huge capital. Now everybody owns stock and many a nerd comes home to play at being a trader at night. TV ads for futures and derivatives trading software, discount brokerages, on line brokerage accounts. Anybody with a 401K or IRA can do it almost for free. Markets behave like mobs, and now the mobs are much bigger, much more amateur. Today we have programmed trading. You don't have to crouch by a ticker tape machine and telephone, a robot does that for you. Now the markets are much more unstable, with robots triggering each other, mobs of robots interacting at electronic speeds across the globe.

The consequences will likely include high interest rates, serious unemployment, recession, stagnant wages, and double-digit inflation (so-called 'stagflation').

Here is one plausible way things could play out over the next year or two:

Continued fiscal irresponsibility causes foreign central banks to begin to unwind their dollar positions, trading dollars for euros and gold. This is actually happening now.

The reduced popularity of dollars and their issuer causes a fall in purchasing US government debt (T-Bills/Bonds).

Unable to finance its deficits, the Fed raises interest rates to attract more T-Note buyers.

High interest rates kill the housing market, home prices fall up to 30-50% in some areas, mortgage defaults and bankruptcies skyrocket. Tight money causes recession, businesses can't get capital to operate or expand.

The Fed attempts to counter recession by increasing the money supply, printing more money. 'Helicopter Bernanky' lives up to his name.

Turns out there's now no balance point between depression and inflation. Hyperinflation results. gold $6,000/oz, gas $20/gal, bread $20/loaf, DVD player $600, house $1,000,000, car $150,000, minimum wage still $8, engineering professional salary still $50,000, jobs: unobtainable. Currency devaluation is the only way government can deal with its debt. Dollar-denominated assets loose 90% of their value.

We become the newest third-world country, a source of cheap labor, manufacturing, and materials at 1/4 to 1/3 our original standard of living.

Things slowly and painfully improve as fiscal responsibility is imposed from without. China and India are the new superpowers.

I consider 1 through 5 as highly likely. All these stages have happened before, and each has in the past resulted in the next. I consider 6-8, hyperinflation, to be a disaster scenario. I don't expect things to go that far. But it is a possibility very much on the table.

Those whose wealth is in the form of dollar-denominated assets may be impoverished. This includes specifically stocks, bonds, and real estate. The Dow will bottom out at something like 1/3 of it's current value.

Most of this should be pretty obvious from the previous discussions. Looking at the pattern of previous recessions/depressions, and factoring in the significantly poorer economic fundamentals of today, I estimate a Dow bottom at 3500, but anything between 1500 and 5000 would be no surprise. The 2000 crash affected tech stocks worse than the broader market. This next event will not be so selective. Whether we end up in a recession or a hyperinflation scenario, regardless of the dollar valuation of your assets, their purchasing power, the only thing that really matters, will fall to 1/2 -1/3 it's former value. A house will continue to be worth one house. But it will be exchangeable for 1/3 as much gas, electricity, Toyotas, DVD players, groceries, and sports shoes. So: stocks, bonds, real estate, all bad. That's pretty much everything, right? Nope. There is an asset class that will not lose it's value, that will even increase it's purchasing power over the next few years.

We are now several years into a commodities boom. You ain't seen nuthin' yet. For the next 6-10 years commodities will be the big winners. This includes specifically energy, metals in general, and precious metals in particular. Gold will peak to at least $3,000/oz. It may or may not fall back to the 1500-2000 range.

Though this crisis may begin in the US, it will not end there. National economies and financial markets are too interconnected. If the world's largest economy, and it's reserve and trading currency fall upon hard times, the whole world economy will probably go down with it. If a country backed it's currency with some commodity, like oil or gold, it might survive relatively unscathed. But none of them do. They are all fiat currencies. Real money represents wealth. A gold warehouse receipt, the deed to an acre of land. They are a promise to deliver something of value. Fiat money isn't really money at all. It represents debt. Worse yet, it isn't a promise of anything in particular, an IOU without an amount.

When we fall into a global recession (it's not a question of if, but of when and how bad) the smart money gravitates to things that have intrinsic value independent of monetary fluctuations. The world appears to swing back and forth between a stock market boom, and a commodity boom. Earlier, I said there was nothing obvious to pick up the slack from the faltering housing boom. That's not completely true, though most institutional investors don't seem to be talking about it. We have now entered a commodity boom. They tend to last about 10 years (though there are reasons to believe this is speeding up). The proof of this is seen in gold, the king of commodities. But you can also see it plainly in silver, the platinum group metals, copper, oil, and even pork bellies for all I know (metals and energy are all I can speak of with any knowledge).

I first started studying and trading between gold, euros, and dollars in 2002 when gold was 265/oz. Pity I was too poor at the time to more than experiment with a couple of thou. Still, I turned a tidy little profit in my first year, at least on a percentage basis. It may hit 600 tonight. That's an average of 31% per year over the last 4 years. The last time we had a gold 'rush' was in 1980. It spiked to $850 in 4 months. In todays dollars, that's about $2200/oz. The fundamentals are much better for gold now, and I expect more like $3,000/3500. Some 'experts' are predicting $6,000, even 10,000. I don't think so. I hope not, because that would imply a lot of suffering for a lot of people. $3,000 gold will be bad enough, at least for those not holding any.

So convert your dollar-denominated assets to gold-denominated assets.

In case you haven't gotten the message already, this is what I've done and what I'm suggesting you do. Mark Twain said "Put all your eggs in one basket, then watch that basket!". If you're not comfortable with that strategy, then pick some percentage you are comfortable with and go with it. Even the staid conservative Wall Street types are starting to recommend you keep 10-30% of your portfolio in gold now, quite a turnaround from what they were saying just two years ago! “Barbarous relic”, I think was the epithet being bandied snidely about. Remember that these are the folks who in 1998 were recommending you put your life savings into derivatives, futures, and tech stocks.

In November 2004 I converted my IRA to gold at $445 and predicted $500 within the next year. In December 2005 it hit $500 and kept on going. Hot dang, nailed it on the nose. 2006 will be harder to call, at least on the upside. This January I predicted at least 650 by year's end, likely 700, and no more than 800. Now, 3 months later it's at 596, already about to cross 600, and I'm sticking to my January estimates. This sort of thing will continue for another 2 to 5 years after 2006, rising at least 30% a year in dollar terms. It's more than possible there will be a 4-6 month period somewhere in there when gold goes up 400%, it happened last time in 1980. I figure this is my big chance (my only chance) at retirement.

There are two ways you win from doing this:

You get to beat inflation, which as I said is already a lot worse than you're being told. No matter how much money they print, the dollar price of gold just goes up enough to compensate for the resulting inflation. In this sense, you are not getting any richer, you are just one of the few who avoid getting poorer.

Remember when I said the purchasing power of gold stays constant? That's not exactly true. There's a supply-and-demand thing that happens. When there's a gold 'bubble', like the one in 1980, everybody wants some ... bad. It's all over the media, it's a subject of conversation: “I got some Krugerrands last week”. Your friends are talking about it. They bid the price up, sometimes by a lot. If you bought some before the mania, you can sell it to those who were late to the party and clean up. If you wait until all your friends are talking about it to buy, you loose your shirt. This will happen, the gold bubble, the rush, the mania, the price spike. Or you can just be conservative, buy early, and wait it out. Gold has been significantly undervalued for various reasons, but that seems to be coming to an end. After a severe monetary crisis, people will have a greater appreciation for it as the safest kind of money. In at least the medium term, it will actually have greater purchasing power than it did. Some people believe that, as Nixon said, fiat money is a temporary failed experiment. (Ironically, Greenspan said the same thing until he joined the establishment and presided over the grandest printing spree since the Wiemar Republic era of wheelbarrow money). Remember these words, you will hear them again: "Gold is Money".

I realize some of you folks are still smarting from the NASDAQ bubble. Can't say as I blame you if you're reluctant to get into what you've been told is risky and speculative. Well, make up your own mind, but please do get informed first. Don't take any so-called expert's advice on faith. Except mine of course (kidding). I've been studying this stuff and trading successfully in it for 4 years now and I'm on it all day every day like white on rice. The Wall Street crowd and the financial media are biased against it. The Gold Bugs crowd (which you can read plenty of in the Kitco Commentaries section) are just as biased in favor of it. Take the Gold Bugs with a pound of salt and don't listen to the Wall Street pundits what-so-freakin-ever. They lead us all over the cliff like lemmings in 1999-2002. Never again will I trust someone else to make my investment decisions for me, especially someone who makes a commission on my trades.

Ways to own gold.

There are lots of ways to invest in precious metals. Each has its trade offs. I'll try to cover the high points in the following table.

|

Form |

Spread |

Cost to Store |

Risk of Theft |

Risk of Fraud |

'Political' Risk |

Liquidity |

|---|---|---|---|---|---|---|

|

Specie in hand |

3.00% |

0 |

High |

Nil |

Low |

Fair |

|

Bullion in hand |

3.00% |

0 |

High |

Nil |

Low |

Poor |

|

ETF Shares |

0 |

0 |

Nil |

Nil |

High |

Good |

|

Pool Account |

0.60% |

0 |

Nil |

Nil |

High |

Good |

|

Bullion in Allocated Storage |

0.15% |

1%/yr |

Low |

Nil |

High |

Fair |

|

Mining Stocks (Experts only!) |

???? <1% |

0 |

Nil |

Low |

Low |

Fair |

|

DGC (Digital Gold Currency) |

2.50% |

1%/yr |

Low |

Low |

Low |

Good |

What is this stuff?

Cost to store: (Agio) the custodial fee charged by eg a vault for security, insurance, etc.

Spread: The difference between what you pay for it and what you can sell it back for. The fixed cost of using it as an investment vehicle.

Political risk: In times of crisis governments have confiscated gold-denominated assets at an exchange rate of their choosing. eg the US in 1933.

Specie: Precious metal coin. 1 oz and 1/10 oz are common. The famous Krugerrands are the cheapest gold coins around, readily available, and resellable at about 2% below the current purchase price. These days, just hold for a month and sell them back at a profit! Seriously, this is much better than a savings account or CD. Available at gold dealers on line and in your town.

Bullion: Plain bars with identifying marks for source, purity, and weight. 1oz, 10oz, 100oz, 400 oz, 1Kilo are common. Cheaper than specie and smaller spread. Available at gold dealers on line and in your town. Most bullion bars never leave the vaults of the LBMA system, you just take title to them as owner of record. That insures not only their safety, but also their provenance, purity, and weight.

ETF: Exchange Traded Fund. On the NYSE, like stock but conveys ownership of unallocated gold rather than ownership of a company. Cheap to trade, free to hold, zero spread (trades at spot) very liquid. Accessible from any self-directed IRA or brokerage account. If you already have one of these, it is the quickest, easiest, and maybe the cheapest way to get your feet wet. See the ticker symbol $GLD (Streetracks Gold).

Spot: The instant going price of gold by the ounce on the world market, varies from moment to moment, sometimes by as much as $10-20 in a day.

Unallocated Storage: You have a claim on X ounces in some vault, but not any specific X ounces.

Allocated Storage: You own a specific, serial-numbered gold object. The difference between allocated and unallocated storage matters mostly to the paranoid. Probably only relevant if the custodian falls prey to theft, fraud, or serious mismanagement.

Pool account: Unallocated storage usually managed by a bullion dealer, easily exchanged for cash or physical gold and back. Very cheap, convenient way to invest in bullion. Kitco is the biggest bullion dealer in the world, or at least the best known. They have pool accounts. Check them out at http://kitco.com/. Kitco is a huge information-rich site, but don't believe everything you read in the commentaries there, though it's must-read stuff for the serious gold investor.

DGC: Digital Gold Currency. Like money in a sort of checking account, but measured in grams instead of dollars. You own real but unallocated gold in vaults all over the world. You can make payments to other users instantly, irreversibly, anonymously, by the kilo or by the milligram. You can use it like a credit card at some online merchants. You can hook it up to a debit card and use your gold to buy stuff at the grocery store, gas station, hardware store, and get cash at ATMs. This is really, really cool, and the future of money. egold is the biggest ($40,000,000 worth of gold), oldest (10 years), most famous. See egold.com . There are several other established and reputable ones. There have also been several ripoff DGCs but they didn't last long. The 4 main ones are 3-10 years old, they and their operators are well known and trusted. There is usually a tiny transaction fee. You exchange DGCs for national currencies at one of many on line exchangers that specialize in this for fees between .3% and 3%. This is a deep subject and the topic of a whole nuther newsletter.

Gold collectible coins: Don't even think about it. The numismatic value of rare gold coins can almost never be recovered. The so-called collectible precious metal coins sometimes hawked in TV and print media are various kinds of ripoff. Stick with the good old common Krugerrands.

Mining Stocks: Don't even think about it. Very high profit potentials, very high risk. Successful investors spend lots of time researching companies, their current projects, their latest news, what the local dictator is up to, and so on.

Silver: Usually moves up and down with gold but further and faster. More volatile and sometimes does the very unexpected. In the long run though, it has even better prospects than gold. This would actually be a good time to buy some silver bullion. It's at $12 now and on the way up to at least $16, and maybe $20 by year's end for various reasons. Don't mess with silver coin, it's not worth it as an investment vehicle.

Fiat: As in fiat currency. From the latin for fact. Ironically it refers to something that has no basis in fact but is accepted as true by declaration, by fiat. A fiat currency has no intrinsic value, whereas a gold-backed currency is redeemable for something of known value, like a gram of gold. Governments are addicted to fiat money because they can make as much as they need at zero cost and no limit. Doing so constitutes a clandestine tax on your citizens, who must use it, and a means of exacting tribute from other countries who hold it as a reserve currency, a trading currency (eg for oil), or as debt you owe them.

Well, that about wraps things up for now. I hope you have found this educational, or at least interesting. Let me know what you think.

Wavyhill – January 2006

Links and Charts

Charts comparing gold to other investments

"The End of Dollar Hegemony", HON. RON PAUL OF TEXAS Before the House Feb, 2006

Sugar-coating the economic indicators

Comodities index, last 2.5 yrs

Inflation-adjusted DOW, 2.5 yrs

{kind=link}

{kind=link}